22 November 2023

CSDDD vs CSRD: Understanding Sustainable Business Dynamics

Discovering the Corporate Sustainability Due Diligence Directive (CSDDD) reveals a crucial shift in how companies handle responsibilities. By 2024, companies must meet their corporate responsibility and protect the environment as part of the European Green Deal.

CSDDD requires companies to deal with environmental compliance, supply chain transparency, and negative environmental effects. This overview compares it to the Corporate Sustainability Reporting Directive (CSRD). It highlights their different but complementary roles in promoting sustainable business practices.

What is CSDDD ?

The CSDDD makes sure that businesses globally stick to the same rules for how they treat people and the environment. Companies must carefully address potential harm to human rights, the environment, and their operations, subsidiaries, and supply chains.

This upcoming directive, set for adoption in 2024, marks a significant change. Requiring companies to take more responsibility and actively address societal and environmental issues will be necessary.

CSDDD: Sharing Responsibilities in the Green Deal Era ?

The CSDDD is a crucial part of the European Green Deal, which is a collection of policies started by the European Commission. The EU Green Deal aims for a minimum 55% reduction in net greenhouse gas emissions by 2030, with the ultimate goal of achieving a climate-neutral Europe by 2050.

Specifically, the CSDDD plays a crucial role in ensuring that companies actively fulfill sustainability mandates outlined in directives like the Corporate Sustainability Reporting Directive (CSRD) and Sustainable Finance Disclosure Regulation (SFDR). It serves as a mechanism to compel companies to not just report on sustainability tasks but actively engage in implementing them.

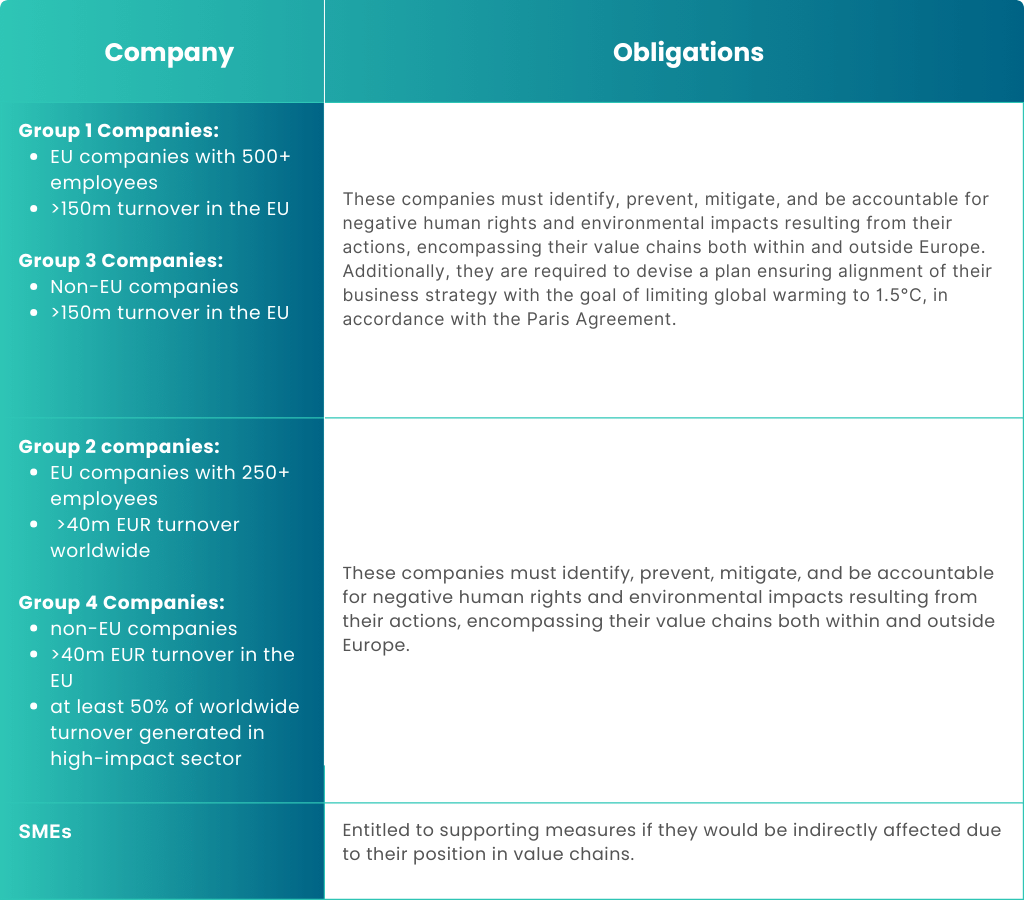

Who Must Comply and When: Scope and Timeline of CSDDD

The CSDDD has different responsibilities for different types of companies.

Every company must identify and stop all negative impacts on human rights and the environment caused by their actions. Every company must do its best to fulfill its responsibilities. To illustrate, this includes creating and implementing preventive action plans, obtaining contractual guarantees from key business partners, and ensuring compliance.

Moreover, companies falling within the directive’s purview, particularly those with turnovers exceeding 150 million Euros (group 1 & 3 as detailed below), are mandated to devise strategies. These strategies should align with limiting global warming to 1.5 °C, in accordance with the Paris Agreement. Those that recognize climate change as a significant risk or impact should include emission reduction targets in their operational blueprints.

Another key aspect of the proposal is assigning responsibility for sustainability at senior level. Directors of EU companies will be responsible for drafting and overseeing due diligence protocols that are seamlessly integrated into corporate strategy.

The CSDDD Timeline

Proposed by the Commission in Feb 2022, the European Council’s finalized approach in Dec 2022 narrows the scope. The MEPs, still deciding, lean toward widening the scope. Trilogue negotiations are expected in late 2023 aiming for adoption by 2024. Rules won’t apply before 2025 earliest. Click here for more information from the EU.

What is CSRD and who must comply ?

The Corporate Social Responsibility Directive (CSRD) by the EU makes big companies in Europe report their sustainability efforts, replacing an older directive for clearer and more consistent reporting. It focuses on environmental, social, and governance (ESG) performance to aid decision-making and trust in the market.

New EU standards are being set for adoption by 2023 and mandatory by 2025. While there’s no direct global equivalent, global efforts are ongoing for universal sustainability reporting standards.

When it comes to complying to the CSRD, CSRD applies to ‘large undertakings,’ which include EU and non-EU subsidiaries, meeting any of the following criteria: total assets over EUR 20 million, net turnover above EUR 40 million, or 250+ employees (see the full requirements list). These enterprises are mandated to provide comprehensive sustainability reports, a key component of which involves disclosing their greenhouse gas emissions data (read more about greenhouse gas reporting here).

The CSRD demands more than just formalities. It digs deep into a business’s environmental and social impact, showing the EU’s strong dedication to sustainability. Through strict enforcement using fines and sanctions, it pushes companies to report thoroughly and on time, setting a new standard for sustainability reporting in Europe.

CSDDD vs CSRD: Differentiating Sustainable Business Directives

The CSDDD and CSRD present distinct objectives in promoting sustainable business practices. CSDDD centers on fostering environmental and social responsibility through a focus on due diligence, demanding companies actively engage in identifying and addressing adverse impacts.

In contrast, CSRD emphasizes transparent reporting for European entities, compelling them to openly disclose their sustainability practices. CSDDD places a strong emphasis on due diligence, stressing proactive measures, while CSRD’s primary focus lies in robust reporting mechanisms. The synergy between the two directives encourages companies falling under both to integrate due diligence efforts with transparent reporting, fostering a comprehensive approach to sustainable business practices.

Conclusion: Embracing Sustainable Corporate Practices

In the evolving landscape of corporate responsibility, the Corporate Sustainability Due Diligence Directive (CSDDD) emerges as a transformative force, propelling companies toward heightened accountability and proactive environmental stewardship. Complementary to this, the Corporate Sustainability Reporting Directive (CSRD) underscores transparency and comprehensive reporting.

As these directives converge, a harmonized approach emerges. Businesses are required not only to disclose sustainability efforts but also to proactively engage in due diligence. The synergy between CSDDD and CSRD paves the way for a new era of sustainable business practices. Responsibility and transparency intertwine for a greener, more conscientious corporate world.